When WeWork filed bankruptcy last year, the reactions fell into two general buckets.

On a business level, the commercial real estate folks brought a “told you so” energy, calling this the end of flexible office space. On twitter, it was mostly jokes about former CEO/guru-preneur, Adam Neumann, poking fun at the company’s unchecked growth, sustained by freely flowing investor money, and boozy office vibes.

The bankruptcy lawyers had a different take. If current operations were struggling with past bad decisions, there was an obvious path for the company to right-size, by selective assumption and rejection of leases under 11 U.S.C. § 365.

That’s exactly what happened, as WeWork expects to emerge from the chapter 11 having negotiated approximately $8 billion (more than 40%) in reductions in rent obligations.

In a typical bankruptcy, a tenant usually is presented a “take it or leave it” choice on leases. Not WeWork. Whether it was a function of a bad CRE market or the scope of their leases, WeWork used chapter 11 to negotiate lots of concessions from its landlords.

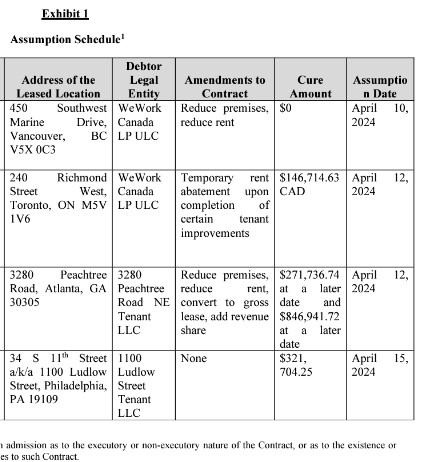

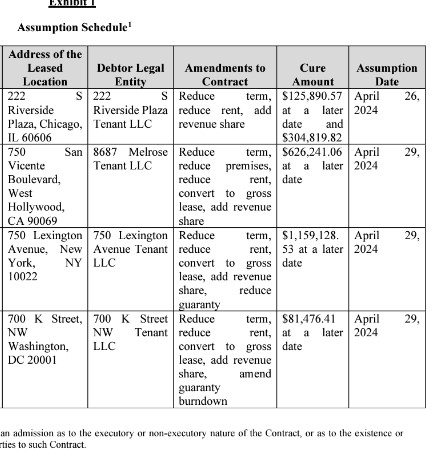

A survey of recent “assumption” orders shows rent reductions, premise and term reductions, conversions to “gross” lease terms, and modifications to guarantees.

Sure, landlords can say “no” to changes like this, but these landlords aren’t.

It’s a smart move, and an indication that serious business people are in charge.

As a tenant of WeWork, I can confirm that the days of booze and debauchery are long gone. In fact, I’d say that they’ve over-corrected. (Ask me about the short-lived decision a few years ago to remove trash cans from individual offices.)

What is in store for the Nashville locations? We don’t know yet. My review of the Bankruptcy Court docket suggests that the debtor has taken no action on the four locations in Nashville.

Pursuant to an Order signed by the Bankruptcy Court on April 29, 2024, the current deadline for these decisions is June 3, 2024. So far, they’ve dealt with only a fraction of the landlords, but I expect lots of activity over the next month.

We’ll know the future of the Nashville locations soon.