When a lender refers me a deed of trust for foreclosure, there are a lot of things I immediately look for. Is the deed of trust recorded? Is this recording in the correct county? Is it signed? Is the collateral description correct? Does the deed of trust even allow foreclosures? (You’d be surprised how often these easy parts get messed up.)

Finally, are the borrower’s redemption and exemption rights waived?

These last ones are easy to overlook, but really important. In fact, I’ve never foreclosed real property on deed of trust without those waivers.

Remember, deeds of trust are contracts between a borrower and a lender. In Tennessee, when borrowers sign a deed of trust, they’re not just pledging their property as collateral—they’re often agreeing to give up certain statutory protections that would otherwise apply if things go sideways.

Two of the most important rights are the right of redemption and the homestead exemption.

The right of redemption, found in Tenn. Code Ann. § 66-8-101, would otherwise allow a borrower two years to reclaim the property after a foreclosure sale by paying the debt. This right to “buy back” the property would hardly ever be exercised, but the mere fact that it existed would cloud the post-foreclosure title and limit the re-sale value of foreclosed properties. This waiver allows the lender (or foreclosure purchaser) to obtain immediate, final title upon completion of the foreclosure sale, eliminating post-sale uncertainty.

The homestead exemption, at Tenn. Code Ann. § 26-2-301, is designed to protect a portion of a homeowner’s equity from creditors. When things go absolutely wrong for a homeowner and they lose their house, the law allows a borrower to protect up to $35,000 before it goes to certain creditors.

As indicated in each of these statutes, both of these rights can be waived in a deed of trust, allowing a mortgage lender the ability to foreclose with clear title.

The absence of these waivers do not prevent a sale, but they drastically change the outlook for the foreclosure process.

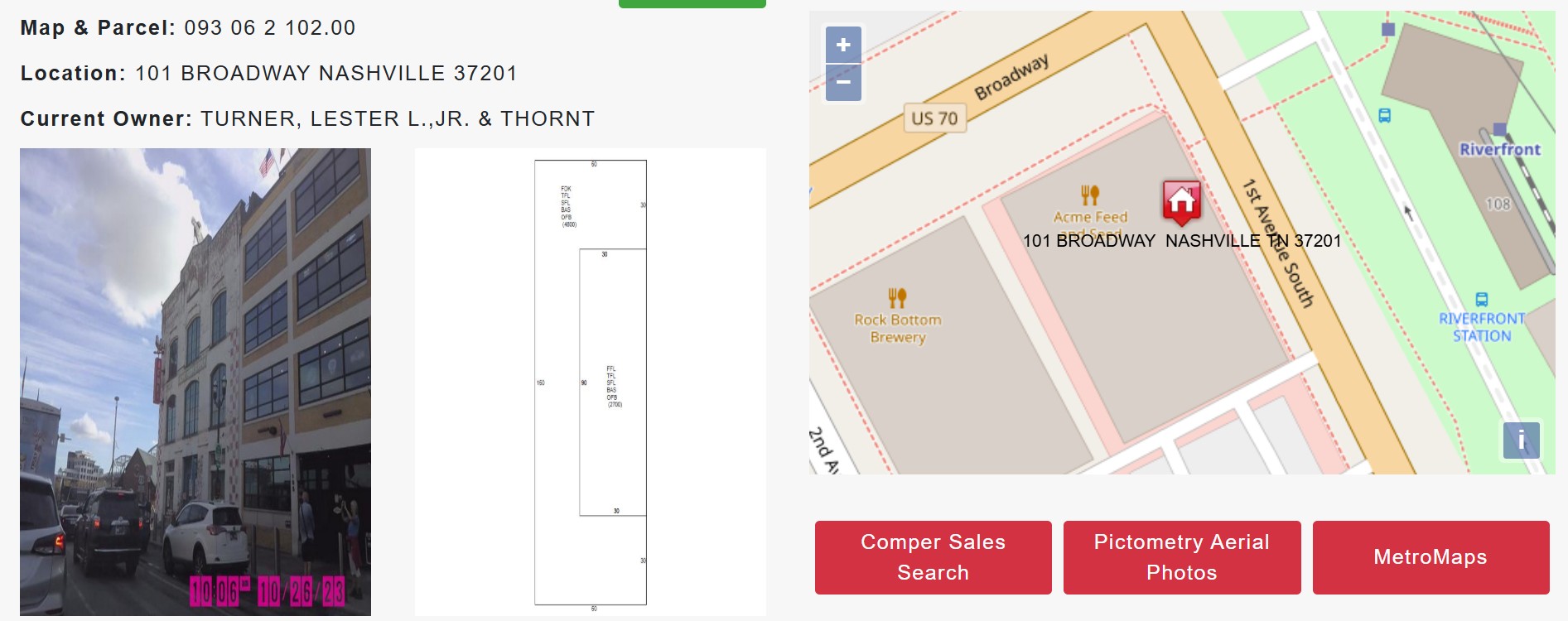

That’s great for the property owners’ balance sheets, but it’s bad news when the Metro Nashville Assessor starts paying attention. (Increases in tax appraisals generally mean higher taxes.)

The public response has been mixed. Lots of people won’t ever feel sorry for somebody whose property value goes up $40+ million dollars (and would fetch far more in a private sale), but those people are missing a key point: Tom Morales doesn’t own the property, per the Quitclaim Deed.

Why, then, would a renter care about the property taxes?

My guess is that he probably signed a triple net lease (often written as “NNN”).

In simple terms, a triple net lease is a lease where the tenant pays not just “base” monthly rent to the landlord, but alsoall of the property’s operating expenses: real estate taxes, insurance, and common area or maintenance costs. In short, the landlord owns the building, but, per the lease, the tenant agrees to pay all of the expenses of the building, usually in 1/12th increments throughout the year as “additional” rent.

If you don’t work in the commercial leasing realm, it probably blows your mind to think that, as a tenant, you’d be responsible for all of the expenses of a property. Why not just buy the building yourself?

It’s a common leasing structure. From the tenant’s perspective, they can operate out of property, without the cash, credit, or long-term obligations of purchasing an expensive building. Acme Feed and Seed may not have had the credit (or desire) to own a $50 Million property, but it can get it via lease. And what a property it is: On New Year’s Eve, nearly 250,000 people rang in the new year at Acme’s front door, with TV and media coverage you can’t buy.

From the owner’s perspective, a deal like this ties up lots of cash or credit on an fixed asset, but, at least, they don’t come deeper out of pocket for the operating expenses. It sounds like a great deal, sure, but being a landlord still carries risk. Ever hear of a bar going out of business and being vacant? Who pays the mortgage, taxes, and expenses in that situation?

At the end of the day, a commercial lease is a contract, and the two parties are free to agree to whatever they want in a lease. They can allocate taxes, insurance, and maintenance responsibilities in any way, and a Tennessee court will hold them to that bargain, no matter how unfair the unforeseen results can be. A contract will be enforced according to its plain language.

With that in mind, for any tenant considering a triple net lease on a property with potential for this sort of wild change, I’d recommend that the tenant consider a provision to mitigate the risk this could happen.

No landlord would be willing to voluntarily bear this tax increase, especially if the tenant retains all of the use and benefit of such a valuable property. (From the landlord’s perspective, the tenant is, now, paying under-market rent, as if the building was still worth a paltry $10Million, right?)

Instead, this lease could have included a provision that allows the tenant to opt out and terminate the lease, if the tenant could prove this increase in the tax cost was a material change. In that situation, the tenant would have an option to get out of the lease and, on the other side, the landlord would be freed from “the burden” of being bound by an under-market lease and could, then, attempt to enter into a new lease based on the $50MM valuation or capture the value via sale. (In short, the landlord would probably happily terminate the lease and see what the free market says about all of this.)

Without that, a tenant can only hope the landlord will pitch in and help with this cost. If I had to guess, all of this hit the local news after the landlord declined to pay the tax bill.

Broadway has changed a lot since Acme first opened their doors 15 years ago. Even the best commercial real estate attorneys could not have foreseen this when drafting this lease, but it’s something to think about on the next honky-tonk lease.

The practice of law is “form” driven. That means that, once a lawyer drafts a really good document, she tends to go back to that document the next time that same issue comes up.

This is particularly true with foreclosures in Tennessee.

Tennessee statutes strictly define what must be included in a foreclosure advertisement at Tenn. Code Ann. § 35-5-104. As a result, a smart foreclosure attorney might start with an old form foreclosure notice, but then compare that against the statute’s checklist, and use that revised document as a form for all of his future foreclosures. (A dumb attorney would just run with whatever is in the form–or what AI says–and not doublecheck it against the law.)

With a little bit of detail work on the front end, a savvy lawyer has a form document that will guide him for years…until the law changes.

The TL;DR version is that the newspaper publications have been reduced from 3 times to 2 times and, now, foreclosing parties must post the notice with a “third-party internet posting company.” See Tenn. Code Ann. § 35-5-101.

If you are updating your form, however, you need to dig in on that other statute. There’s a discrete change in the sale notice requirements.

It’s at Tenn. Code Ann. § 35-5-104(a)(7), which adds that the sale notice “shall…[i]dentify the website of the third-party internet posting company that posts an advertisement pursuant to § 35-5-101(a)(2).”

I’m posting this warning because, candidly, I didn’t catch this change in my first reading of the new statutes. Instead, when I was preparing my first “post-July 1” sale notice, I went online and read other recent advertisements, to see what changes other law firms had made on their forms.

In doing that, I noticed this text in many of them: As of July 1, 2025, notices pursuant to Tennessee Code Annotated § 35-5-101 et seq. are posted online at https://foreclosuretennessee.com by a third-party internet posting company.

That’s weird, I thought. Why are they saying that? That’s when I dug in on § 35-4-104 and found that little change.

Non-judicial foreclosures in Tennessee are tricky. You have to comply with both the letter of the statute exactly and with the terms of the relevant lien instrument. In short, you have to be awesome at paperwork.

Big-picture compliance with the changes in Tenn. Code Ann. § 35-5-101 is easy. This post is a reminder that there’s a very little change in Tenn. Code Ann. § 35-104 that could have a big impact on your sale.

This was the first time that the Tennessee legislature limited a creditor’s collection rights after a foreclosure. And the text was pretty ambiguous.

The statute created two general scenarios where a debtor could fight efforts by a creditor to obtain a deficiency judgment after a foreclosure:

Where the debtor can make “a showing of fraud, collusion, misconduct, or irregularity in the sale process” (see Tenn. Code Ann. § 35-5-117(b)); or

Where the debtor can “prove by a preponderance of the evidence that the property sold for an amount materially less than the fair market value of property at the time of the foreclosure sale” (see Tenn. Code Ann. § 35-5-117(c)).

At the time, foreclosure attorneys focused on what “materially less” than “fair market value” meant. The legislative history of the statute revealed that the lawmakers pulled that phrase from divorce law, where a “material change in circumstances” could impact child custody decisions. (Not much guidance on foreclosure cases.)

But what about the part we all overlooked, Tenn. Code Ann. § 35-5-117(b)? We took that part for granted because, seriously, does any lender or foreclosure attorney commit fraud, collusion, misconduct, or irregularity in the sale process?

I don’t ask this in a rhetorical way. It’s an interesting question, and, in light of customary foreclosure practices in Tennessee, I think it’s ripe for litigation.

Here’s an example, which you can try at home. Grab your local newspaper (assuming one still exists in your area), and look for the foreclosure notices. Pick the first one you see, and call the foreclosure attorney and see what happens.

In my experience, it’s likely that:

The attorney/staff will never answer your call/email.

The attorney/staff will not call/email you back.

If you do hear back, you will not be provided with any information other than what is in the sale notice.

In many situations, you will not even get confirmation whether the sale is proceeding or not.

There will be sale terms announced in the minutes before the sale, but those are only rarely shared with interested parties in advance. Things like: Whether buyers need to bring cash. If so, how much. When will closing happen. Whether buyers need be pre-qualified.

These are fundamental questions that any reasonable bidder would expect to be provided. If an interested party doesn’t get these answers in advance, then they simply will not show up or, if they do, will be unprepared to bid. This uncertainty and failure to communicate leaves foreclosure bidding to the low-ball bidders, who make their money by exploiting the ambiguity (and low bid prices).

The failure to respond to interested parties’ reasonable questions will chill interest in a sale and will reduce the number of potential bidders. This could rise to the level of a violation of the foreclosure trustee’s duties under the Deed of Trust and could, possibly, render the sale “irregular.”

Foreclosing lenders in Tennessee should consider subpart 117(b) and how they or their counsel handle sales. Sure, no lender thinks their sale is “irregular,” but, on the right facts, you never know how a court will rule.

Maybe it’s a harbinger of a worsening economy, the lack of new commercial lending, high interest rates scaring buyers away, or just that secured lenders are sick of being patient, but Nashville is seeing more commercial foreclosures lately.

Right now, things seem different. Borrowers don’t have access to the same borrowed funds they had over the past 2-3 years. The exuberant “new money” buyers pouring into the market seem to have slowed down. Both the lenders and borrowers can see the “bottom of the river” regarding cash flow and business income.

As much as we’ve been kicking the can down the road on various deals, we keep ending up at the same place, with foreclosure the only remaining exit strategy.

Next week, I have 5 commercial foreclosures set over the course of two days; the week after that, I have 2.

As that post shows, I’ve been wrong for years about the pending explosion in new bankruptcy cases (it’s largely never happened), so maybe I’m wrong about the lack of bankruptcy attorneys.

In common parlance, a “squatter” is a person who takes possession of property without any rightful claim. In my mind’s eye, I picture a modern-day pirate, moving into your home and declaring “This is MY house now!”

In my 25 years of eviction and property litigation, I’ve actually never dealt with a squatter. I’ve certainly never perceived it to be a problem that justified special legislative attention.

Effective July 1, 2024, we now have Tenn. Code Ann. § 29-18-135, titled “Limited alternative remedy to remove unauthorized persons from residential real property.” This statute is added to the end of Title 29, Chapter 18, which are the eviction and detainer statutes.

This new statute creates a process by which a property owner can, by filling out a checklist form, direct the Sheriff to remove an “unauthorized person” from the property, without a court proceeding.

By its clear text, “a property owner…may request from the sheriff of the county in which the property is located the immediate removal of any person unlawfully occupying a residential dwelling pursuant to this section if…[a]n unauthorized person has unlawfully entered and remains on the property owner’s [residential] property” and “[t]he unauthorized person is not a current or former tenant…” (this is heavily paraphrased, so be sure to look at subpart (d) in full).

The word “squatter” isn’t in this statute. Instead, the statute deals with “any person unlawfully occupying a residential dwelling” who “has unlawfully entered and remains or continues to reside” on the property and who “is not a current or former tenant…” and “is not an immediate family member of the property owner.”

That’s a pretty broad definition, and it seems to include persons not routinely labelled “squatters.” For instance, wouldn’t a foreclosed homeowner be subject to this statute? They are no longer the “owner,” they aren’t a “current or former tenant,” and if they stay at the property after the foreclosure deed is recorded, the possession is “unlawful.”

In my experience, “squatters” simply haven’t been a bane to Tennessee property owners’ existence. I’m not saying it never happens (and I’m sure that all it takes is one years’ long fight with a squatter to change my mind), but it seems like the existing statutes provide a good remedy, and, at best, this statute puts an awkward amount of judicial discretion into the hands of the local sheriff (who probably would rather all this be decided by a judge).

I have a question I ask clients when they ask me to foreclose on a property.

“Do you want the money or do you want the property?”

Some clients are baffled by the question. They are banks, they’ll tell me, and what are we going with a property? Who is going to evict the tenants, change the locks, make sure the pipes don’t burst, cut the grass and so on? The banks don’t want all that trouble. They want the money back, plain and simple.

But, in a hot real estate market like Nashville, I’ve noticed a new type of lender. I refer to them as “loan-to-own” lenders. They are making loans secured by real property, but they sometimes act like property investors.

My hunch is that, when making the decision to extend credit, the prospect of ending up owning the property is part of these lenders’ motivation in doing the deal. Hence, the “loan-to-own” nickname I give them. When their loans go bad, these lenders are happy to foreclose and take ownership of the land.

These are often lenders of last resort, for a property developer who can’t get credit (or more credit) from a traditional lender. These loans are often at far-above-market interest rates and usually on pretty short repayment terms. The typical customer is a developer who just needs a little bit more money or a bit more time, and who, out of desperation or arrogance, believes that the “big” sale is just 90-120 days away and is willing to overlook the costs and risks.

When the sale doesn’t happen or a payment is missed, these lenders pounce. In some cases, maybe the property developer can figure something out and the loan (and the hefty interest and fees) gets paid.

Or, worst case, the lender presses forward with a lender-advantageous foreclosure, i.e. one in which the lender who wants to win at the sale is the one who gets to set and enforce the sale terms.

Over the last few years, I’ve seen more lenders from Texas, Las Vegas, and California loaning money on development deals in Middle Tennessee. I’ve also noticed more of these lenders foreclosing, taking ownership, and then offering the properties for sale.

Having said all this, I don’t expect (or offer) much sympathy for the cash-strapped property prospectors. It’s simply an interesting development in the gold-rush ecosystem of the modern Nashville real estate market.

I saw something at a Nashville foreclosure yesterday that I hadn’t seen in years.

A luxury, high end house in a great neighborhood was auctioned, and nobody showed up to bid. The Lender bought it back at a credit bid. (In the spirit of disclosure, it was a $2MM+ credit bid. They weren’t quite giving it away, but this is Nashville).

It reminded me of foreclosures in the Great Recession, when you’d stand on the courthouse steps, reading a foreclosure sale notice to nobody and, invariably, your bank would become the new owner of the property.

Back in 2008, lenders were dealing with the after-effects of an easy-money market. Builders with good credit built too many houses, too fast, and the market had a glut of inventory, with no buyers in sight.

The lack of buyer-credit meant that new sales couldn’t keep up with the builder’s debt obligations. It was sort of a ponzi scheme, as sales of today’s houses were necessary to pay for yesterday’s construction costs. When the money level dipped, lots of partially built spec homes got foreclosed, after the builder’s new money ran out and they were defaulted or simply gave up.

I thought about 2008 yesterday.

As much free-flowing money as there’s been in the Nashville retail-buyer and foreclosure market over the last 4-5 years, it was a surprise to see that sale fall flat yesterday. In the last year, I’ve done foreclosures in Nashville with 20-30 bidders present. But, on a sunny Thursday, with a Belmont-Hillsboro Village house on the block, and there are no bidders, buyers, or bankers willing to refinance?

Could this be a leading indicator of a larger problem in Middle Tennessee?

The signs are there. This exuberant builder refurbished a modest 1920s bungalow, to construct a 8,712 square foot, 2 car garage, 5 bedroom, 8 bath outlier, originally offered for $3,675,000 (estimated monthly payment of $20,012). The house isn’t entirely finished–it looks like contractor work on the new backyard pool and outdoor area has stopped.

The builder has more than a dozen projects throughout Nashville, in similar stages of “in progress” construction. The builder also has a number of pending foreclosures and twice as many pending lawsuits. The construction on a number of the sites seems to have simply stopped.

Just a few years ago, just one high-end property selling for top-dollar would have bought an over-extended builder a few months, finished another project, and lead to another sale, but it seems like the buyer market has waned as well. When both buyers and banks get cautious, risky bets come due.

There are a number of peculiarities here that may make a broad-takeaway unreliable. But, with that caveat, I’m seeing lots of the same issues and patterns that we saw in 2008.

Plus, by mid-morning, I’d learned that the developer filed a Bankruptcy. Just like they did in 2008.

When a mortgage or judgment gets paid off, the creditor has to release its lien. It’s not only common sense, but it’s a duty imposed by Tennessee statute (seeTenn. Code Ann. § 66-25-101).

It’s an easy process to prepare a Release of Lien and record it with the register of deeds. Also, it’s not particularly expensive. Depending on how many pages the release is, the fee can be as little as $12.00.

Not too onerous for a lender who just got paid in full, right?

Well, not so fast. Ask any of my creditor clients, and they’ll tell you that “paid in full” means “fully paid, including that release fee.” When I get a payoff request on a deed of trust or judgment lien, I generally include a line for the $12.00 release costs.

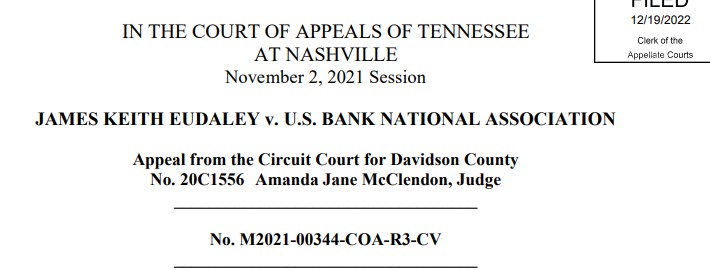

Not anymore, in light of a December 2022 Tennessee Court of Appeals opinion, Eudaley v. U.S. Bank Nat’l Ass’n, No. M202100344COAR3CV, 2022 WL 17751378 (Tenn. Ct. App. Dec. 19, 2022). In that case, the mortgage lender got paid in full, recorded the release, and sent a bill to the borrower for $12.00. In response, the borrower filed a class action lawsuit in Davidson County Circuit Court, arguing that, per Tenn. Code Ann. § 66-25-106, “[a]ll costs … for registering a formal release[ ] shall be paid by the holder of the debt secured by the … deed of trust.”

Despite the very clear statutory text, the trial court dismissed the case after finding that federal law allows such fees and preempts the state law. The Court of Appeals affirmed, but not before providing some useful guidance to other lienholders (who may not have a federal banking regulation to hide behind).

Specifically, the Court wrote that “§ 66-25-106 prohibits holders of debt from seeking reimbursement of costs associated with recording a release of a deed of trust” because “[t]he debt holder’s obligation to record a release only arises if the debt has been paid in full or satisfied, indicating that nothing further is owed to the debt holder.” In affirming the trial court’s dismissal, the opinion makes clear that the lienholder bears those costs and can’t seek reimbursement, but, nevertheless, “that prohibition is preempted by federal law when the debt holder seeking reimbursement is a national bank.”

So, what if you’re not a national bank? Tenn. Code Ann. § 66-25-106 applies, and the creditor must chalk up $12.00 as the cost of getting paid.

What about other sorts of liens, like judgment liens or mechanic’s liens? § 66-25-106 seems to apply to any lienholder, but the judgment creditor may nevertheless have an argument that the release fees are “costs of collection” or allowed court costs/discretionary costs.

Either way, this December 2022 opinion provides pretty compelling authority to support a lender’s decision to simply record the release and write off the $12.00. In a very creditor-friendly state like Tennessee, Tenn. Code Ann. § 66-25-106 is an outlier, but this case is a very good reminder that it exists.

In 95% of Tennessee foreclosures, the foreclosing lender has appointed a substitute trustee to conduct the sale but, of those, about 10% mess the process up and conduct a defective sale.

First, some background. When a borrower grants a lien pursuant to a deed of trust, the real property is conveyed to a specific trustee named in the instrument “to hold title to the property in trust” pending the repayment. If there is a default, the trustee can later sell and convey title to the property.

These trustees are generally a closing lawyer or trust officer at the bank, but they are rarely the same lawyer who does the foreclosures for the bank. (Note: There’s no reason that they can’t be same.)

Later, if the bank decides to foreclose, one of the first steps is to appoint a “foreclosure” lawyer to be the successor trustee under the deed of trust. This is done by simply preparing an Appointment of Substitute Trustee, having the lender sign and notarize it, and recording it with the register of deeds in the relevant county.

Sounds easy, right?

Here’s where the mistake happens. When the decision to foreclose is made, the bank (or the lawyers) sometimes rush it out the door and start the foreclosure either before the Appointment of Substitute Trustee is signed or before it is recorded. (Spoiler: One of those is fatal to the foreclosure.)

Under Tenn. Code Ann. § 35-5-114(b)(3), if the Appointment is not recorded by the first publication date, there is specific “savings” language that must be included in the foreclosure sale notice. This text says, basically, that, even though the appointment hasn’t been recorded, the lender “has appointed the substitute trustee prior to the first notice of publication as required by Tenn. Code Ann. § 35-5-101…”

As a result, it’s still a valid sale, as long as that text is included. But, as this text also suggests, it may not be a valid sale if the actual Appointment of Substitute Trustee was not signed until after the foreclosure sale notice was published. If that’s the case, a court may find that the successor trustee was a stranger to the property at the time he or she issued the sale notice. (And strangers have no power to start a sale.)

Tennessee foreclosure statutes are non-judicial, which means it’s all just paperwork, but there’s an exact sequence of steps that must be followed.

This particular error is an easy one to avoid, but also an easy one to make. Many creditors want to foreclose quickly, which requires the lender and its counsel to satisfy strict publication deadlines to get the sale notice published and to obtain a sale date.

In doing so, they can often overlook the necessity of getting the initial paperwork executed in advance (whether it’s the rush of getting the sale notice to the local newspaper or the simple hassle of finding a notary for the appointment of substitute trustee).

As we have seen in recent cases, the failure to follow the technical requirements of Tennessee law and deeds of trust can result in a challenge to a foreclosure. It’s all paperwork, but make sure you get it right.