When WeWork filed bankruptcy last year, the reactions fell into two general buckets.

On a business level, the commercial real estate folks brought a “told you so” energy, calling this the end of flexible office space. On twitter, it was mostly jokes about former CEO/guru-preneur, Adam Neumann, poking fun at the company’s unchecked growth, sustained by freely flowing investor money, and boozy office vibes.

In a typical bankruptcy, a tenant usually is presented a “take it or leave it” choice on leases. Not WeWork. Whether it was a function of a bad CRE market or the scope of their leases, WeWork used chapter 11 to negotiate lots of concessions from its landlords.

A survey of recent “assumption” orders shows rent reductions, premise and term reductions, conversions to “gross” lease terms, and modifications to guarantees.

Sure, landlords can say “no” to changes like this, but these landlords aren’t.

It’s a smart move, and an indication that serious business people are in charge.

As a tenant of WeWork, I can confirm that the days of booze and debauchery are long gone. In fact, I’d say that they’ve over-corrected. (Ask me about the short-lived decision a few years ago to remove trash cans from individual offices.)

What is in store for the Nashville locations? We don’t know yet. My review of the Bankruptcy Court docket suggests that the debtor has taken no action on the four locations in Nashville.

Pursuant to an Order signed by the Bankruptcy Court on April 29, 2024, the current deadline for these decisions is June 3, 2024. So far, they’ve dealt with only a fraction of the landlords, but I expect lots of activity over the next month.

We’ll know the future of the Nashville locations soon.

A recent case involving Deja Vu Showgirls Nashville (warning: do not click that link) offers a useful map for a judgment creditor to follow where a garnishee fails to answer a wage garnishment.

In the case, One Main Financial Group, LLC v. Edward Hackney, Jr. (Davidson Co. General Sessions Docket No. 23GC8323), the Plaintiff served a wage garnishment on “Deja Vu Showgirls, Attn: Payroll.”

In the Sessions case, there was no answer filed, and Plaintiff filed a Conditional Judgment, asking that the full $14,000.56 judgment against Hackney be made a judgment against Deja Vu. Once a conditional judgment is signed, the court then sets a final hearing on whether to enter a final judgment against the non-responsive party.

When Deja Vu failed to respond in any way to the wage garnishment or the conditional judgment, the Court granted a final judgment against it for the underlying debt.

Unsure of where Deja Vu banks or holds assets, the Plaintiff issued a levy instructing the Sheriff to seize the “Cash Box.”

Plaintiff’s logic was sound. A few weeks later, the Sheriff went to the establishment (on a Saturday!), seized all available cash (well, the cash up to $14,634.00, the amount owed under the Judgment), and paid the funds to the Court Clerk.

Some thoughts?

Don’t ignore wage garnishments. Ever. Who knows if Edward Hackney works at Deja Vu or, even if he did, would he have been paid $14,000 during the garnishment. Due to Deja Vu’s failure to respond, the actual facts are irrelevant; Deja Vu became liable for the full debt simply because it never responded.

Was the cash levy valid? A judgment creditor can levy against personal property of the judgment debtor, including cash. This is often called a “till tap,” and it’s a smart move anytime you’ve got a judgment against a debtor with cash in their pockets, in their possession, or in their cash register.

In the end, the best test of collections process is whether it works. Here, Plaintiff got a little bit lucky. The Sheriff served this levy on a Saturday, presumably when the business had ample cash on hand (I actually didn’t realize the civil process unit served process on weekends).

And whoever was manning the cash box didn’t raise any issues related to service or the accuracy of the corporate name issue at any point–whether at the time of the levy or before the money was disbursed. (Looking at the corporate records at the Tennessee Secretary of State, an argument could have been made about some things.)

Sometimes, a little bit of luck makes all the difference.

My advice is to always take as much care in issuing levies as you would when filing a lawsuit. That means getting business name exactly correct. A judgment in this situation is like any other judgment–you have to get valid service of process and party’s name correct.

I’ve heard from a number of lawyers that it’s what they’ve always done, but, nevertheless, it’s nice to have a bit of judicial reassurance.

Back in September 2023, immediately after a trial in Sumner County, I was racing to get the new judgment recorded on land that the judgment debtor had under contract for sale.

As soon as the Judge signed my order, I asked to make a certified copy. Cautiously, because I’ve had judges and court clerks admonish me in the past for even asking for a certified copy of a brand new judgment.

In my case, I had no time to spare.

My Register of Deeds visit was where the real fun started. Within minutes of being handed my certified copy, I was at the Register of Deeds’ front counter.

While I was sitting in the Register’s waiting area, I overheard them discussing a problem they had to deal with.

A Big Law Firm had mailed in a document for recording for the third time, and, once again, the “payee” name on the check was wrong. I don’t know what was written on the check, but it did not say “Sumner County Register of Deeds” (or, I assume, anything close to that).

Twice already, the Register of Deeds had rejected the filing and mailed it back.

As I was sitting there, they were discussing what to do about this third time.

How on Earth does this happen three times? As it turns out, the year before, this AmLaw 200 Big Law Firm had purchased (or, as the marketing people say, “combined with”) a local law firm and checks were no longer written in Nashville or anywhere in Tennessee.

Instead, the checks were written 600 miles away by someone who has probably never heard of “Sumner County” or a “Register of Deeds Office,” and who probably has never met the lawyer (or client) who desperately wanted whatever was being rejected to be recorded.

I have no idea if the third recording got accepted that day, or if the Clerks ever just called the Big Firm to sort it out. I got my recorded judgment lien on the property and left; the rest was not my problem.

So what’s the point of the story? To be clear, I was very amused by it all.

Sometimes, when I am writing my own checks or driving to record my own documents, I miss the old law firm days when I had a person who did all that for me. But, I’m also a control freak who takes his job very seriously, and I would have lost my mind if I had lost weeks trying to record something that kept getting rejected.

Most articles about law firm acquisitions /combinations have the narrative that “bigger is better,” and usually mention “broader reach,” “expanded networks” and “new markets.”

Sitting there that day, with sweaty palms, watching the clock, hoping to get my document recorded before the land could be sold…I was glad to be the guy writing my own checks.

We’re one step closer to answering one of Tennessee collection law’s greatest mysteries: Can a judgment creditor record a copy of its judgment as soon as it is signed by the Judge, or must the creditor wait 30 days?

The question arises under Tenn. R. Civ. P. 62.01, which says that “…no execution shall issue upon a judgment, nor shall proceedings be taken for its enforcement until the expiration of 30 days after its entry…”

For starters, what’s the statutory authority for recording a judgment lien? I look at Tennessee Rule of Civil Procedure 69, which is titled “Execution on Judgments,” and includes all the different ways you can “execute” on judgments (garnishments, levies, sheriff’s sales, liens). This list includes Tenn. R. Civ. P. 69.07(2), “Execution on Realty,” which provides the exact process to record a judgment lien against the judgment debtor’s realty.

And let’s be honest; why would you record a judgment in the first place? Under Tennessee law, the recording of a judgment with the register’s office creates a lien on real property, meaning that the debtor can’t sell, refinance, or transfer the property without dealing with the judgment. It’s a pretty powerful tool to get paid. That’s why you’d record it, and as fast as possible.

If the point is to get paid–and as soon as possible–that looks a lot like enforcement, right? But is that “execution”? Should we also throw around terms like “collection” or “attachment” too?

It’s been a mess because the statutes and rules all seem to use these different terms interchangeably, except when they aren’tinterchangeable.

Faced with this exact issue, the Davidson County Chancery Court had to make sense of these competing terms and concepts. In an Order from February 2, 2024, the Court found the mere act of recording a judgment during the Rule 62.01 stay period “was not premature ….because the filing of judgment lien is not an act of enforcement.”

In doing so, the Court referenced the pleadings filed in the matter, which drew reasoning from Tenn. Code Ann. § 25-5-101(b)(1) and the competing concepts of “final” judgments found in Tenn. R. Civ. P. 54 and 62.01. Further, given the Court’s brief, but specific, factual finding, the Court seems to agree with the opposing brief’s distinction between the acts of recording a lien versus enforcing a lien, arguing that only the latter would violate Rule 62.01. The full Order is attached below.

It’s an important issue that has long vexed creditor rights lawyers, debtor’s counsel, and even court clerks. I’ve had court clerks only begrudgingly provide me with a certified copy of a judgment on the day of entry (and reminding me that I “can’t do anything with it for 30 days”).

This Order and the related reasoning may provide a roadmap for future arguments on this issue, which comes up far more frequently than you’d think.

I watched these trial court proceedings pretty closely, and I’m glad to see a creditor-friendly result. The underlying initial pleadings are also attached below.

A few months ago, I got an unexpected call from a local Sheriff’s Office, late on a Friday afternoon. (Hardly ever always a good thing.)

This Sheriff and I had done a real property “sheriff’s sale” a few years ago that was very successful, and he had one scheduled for Monday that he needed my help on.

“Can a Sheriff’s Execution Sale of Real Property be Continued?” he asked.

The attorneys for the creditor and the judgment debtor were trying to work out a deal, but they were running out of time, but the Sheriff didn’t think he could give them more time.

I wasn’t sure either, so I went with my default answer: “It depends. Let’s talk this out.”

In the end, my advice was: “Under existing Tennessee execution law, he couldn’t: He had to proceed, or the judgment creditor had to call it off. There was no in between.”

Back then, unless the text of a deed of trust expressly authorized a foreclosure postponement, trustees weren’t sure if they could continue a sale. Some trustees included language in their sale notices allowing continuances, making it seem like it was no big deal (but if you if you pressed them on the authority to postpone a sale, they’d usually admit that there was none).

Back then, if a deed of trust was silent on continuance, most prudent lenders tended to proceed with a sale, regardless of whether the parties were negotiating potential resolutions. Tenn. Code Ann. § 35-5-101(f) was enacted to avoid those harsh results and help parties who were trying, in good faith, to resolve disputes and save their homes. It gave them some relief to work out a deal.

So, back to our Sheriff’s Sale. The analogy to foreclosures is apt, because the sheriff’s sale statutes track the foreclosure statutes. If you at Tenn. Code Ann. § 26-5-101, et. seq.–it’s nearly the exact same text. In short, a Sheriff’s Sale is, basically, the same thing as a foreclosure sale, but done by the sheriff.

But, for this blog post, I’ll point out a big difference: There’s no § 26-5-101 “(f)” — the part about the continuances. It’s the same text, except for that section.

Uh oh.

And, of course, there’s never going to be any sort of contract to fall back on, because there’s hardly ever going to be any sort of contract between a judgment creditor and judgment debtor providing any sale terms (as a deed of trust would between a borrower and lender).

Separately, there’s nothing in any other Tennessee statutes–talking about execution, sheriff sales, Tennessee Rule of Civil Procedure 69 or elsewhere–about continuances.

Finally, in talking to the Sheriff, I asked him–in a last ditch effort to see if I could help the parties on his sale get some more time to reach a resolution–whether their case’s Sale Order or Notice of Sheriff’s Sale said anything about ability to continue or postpone the sale? There was nothing at all they could point to.

In a perfect world, we’d have a statute that allows continuances in sheriff’s sales. In a less perfect world, the Court’s Sale Order would allow a continuance. In an even less perfect situation, we’d have a Notice of Sheriff’s Sale that would allow a continuance.

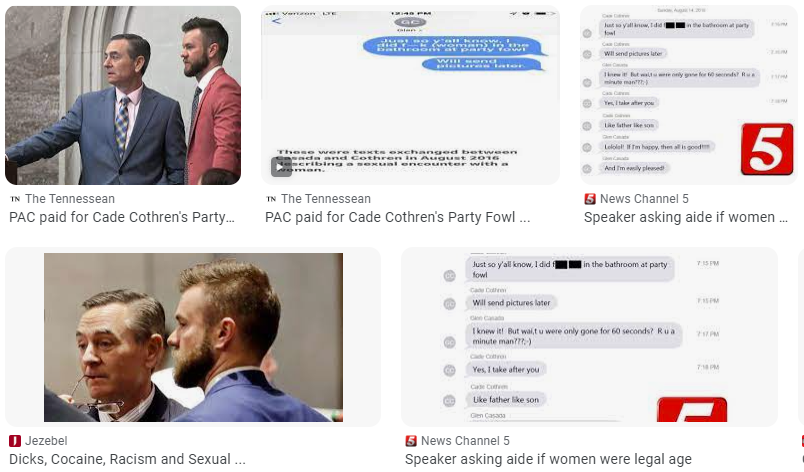

Some of it can be chalked up to schadenfreude: The restaurant was the site of a fairly salacious political scandal involving some of Tennessee’s least likeable politicians in recent memory. Whether it’s echoes of that scandal or its location in the party-centric Gulch, Party Fowl tends to get a bad rap from locals.

The reactions also reveal common misconceptions about how Chapter 11 works. Sure, if a company files a Chapter 11 bankruptcy, something has gone terribly wrong, but it doesn’t necessarily mean the end of the company.

The goal in Chapter 11 is rarely to simply shut down, but, instead, it’s to reorganize and stay in business. This generally involves freezing payments to creditors (unless it’s post-bankruptcy vendor payments), restructuring the company’s debts (i.e. extending the payment terms and, sometimes, paying only a fraction of the amounts owed), rejecting leases (i.e. undoing bad business decisions), and, generally, cut operations and expenses going forward (i.e. downsizing).

At the end of this process, a chapter 11 debtor will propose a plan of reorganization (based on a realistic budget it can handle) to keep its business alive and pay creditors over time.

Most companies continue operations after filing Chapter 11, and the customers will never notice any difference. Party Fowl filed bankruptcy nearly ten days ago, but they’ve been selling hot chicken continuously over the past two weeks.

Party Fowl appears to have some good reasons for filing. Based on their Company Profile (copy below), the debtor told the Bankruptcy Court that COVID was a big disruption with awful timing: They started a bold expansion in March 2020, and those new locations have struggled and drained resources, impaired cash flow, and led them to take out some fairly onerous and high interest merchant lender loans to bridge the gap. The bankruptcy filing allows the debtor stop paying those sky-high rate loans and use the income to right-size the business.

This is a Creditors Rights blog, written by a creditor rights lawyer, so please don’t think I’m going soft here. Based on the pretty extreme “Party Fowl, we hardly knew thee” reactions, I thought a little bit of background could be useful.

And, don’t worry, I’ve got lots of criticisms about the chapter 11 process, but I’ll save those for a later post. (Just wait until I tell you the story about the mega-bankruptcy case that paid the lawyers $100s of millions of dollars in legal fees and costs over 5 years, and the check my client received last month for 1.04% of his claim…)

When I think about my least favorite cases, it’s generally because the client is terrible in some crucial way.

I remember the day I got my own all-time least favorite case. It was about 20 years ago, and my day started with a simple matter in Williamson County General Sessions Court. While I was waiting for my case, there was a dramatic hearing on the docket right before mine.

A contractor had filed a pro se collection lawsuit, and, during the trial, the contractor came with a wild energy, ready to fight. He got into an argument with the lawyer on the other side, threatened the homeowners, had no documents to support his case, and ended the trial by yelling at the Judge (who had ruled against him and told him to hire a lawyer and appeal it, if he thought the decision was wrong).

As the contractor stormed out of the courtroom, yelling at everybody, I remember thinking “I would hate to be that guy’s lawyer.”

In the two hours that it took for me to get lunch and make it back to my office in Nashville, my boss had a new case for me. Yes, it was that guy. He had told his cousin about how he had gotten screwed over by a biased judge and needed a lawyer for the appeal in Circuit Court. The cousin–a client of my firm–recommended my boss, who handed the file directly to me.

I told my boss what I saw in court that day and begged him not to take the case.

I’ll spare you all the details, but that client never got less angry and more reasonable. He was mad at me for asking for paperwork and proof. He didn’t understand why we needed evidence. He was mad at the bills we sent him. He refused to participate in any meaningful aspect of the process. He hated me and questioned everything I said to him about the case. Settlement was never an option. We were going to fight this to the end. My boss took a “hands off” approach.

In the end, he showed up for the trial in Circuit Court, but it was only slightly less wild than the first trial. We lost spectacularly, and my memories of that trial are as vivid to me as my memories of my wedding day and the births of my children.

I tend to think about that case during the holiday season, because, after that trial, I went directly to a real estate agent’s elaborate holiday party in a 6,000 square foot model home in Brentwood (this was the good times, pre-Great Recession). I drowned my PTSD in eggnog.

That may be the greatest benefit of running your own firm. At my old firm, you got handed cases, whether you wanted them or not. Some clients are unreasonable. Some have bad claims. Some can’t afford a lawyer. In a big firm, often you don’t always have a choice. It’s too bad, though, because taking on bad cases or bad clients is an easy way to create unhappy lawyers.

Don’t get me wrong: In your own firm, you will absolutely take on bad cases and bad clients, but it’s different when it’s your own choice. At worst, it’s a lesson you (hopefully) learn from. Having recently closed the last of what I referred to as “The Sinister Seven,” I can assure you that it’s a learning process (ask me about the sequel, “The Terrible Two”). Taylor Swift and I both can benefit from some honest self-reflection.

After three plus years of running my own firm, you would be shocked at how picky I have become (I call it The Client Decision Tree, and I’ll do a full post on that soon). Some lawyers see those initial client calls like a job interview, and I do too: But it’s usually me doing the vetting.

I refer out about three times as many cases than I accept, and it’s been a revelation. Some clients simply make things more difficult, and that can impact your entire practice.

To this day, my engagement letters say “the attorney-client relationship is one of mutual trust and confidence,” and it’s not just filler to distract the client from the hourly rate and retainer. If I get a sense from a potential client that she doesn’t respect my role, the legal process, or trust me (i.e. listen to me), that client never gets an engagement letter.

Life is too short and reputations are too fragile to do work for clients who aren’t a good fit with my firm. Say yes to too many bad clients, and you’ll find you have less time, patience, and space for the awesome clients.

Yesterday, the Tennessee Court of Appeals issued a new opinion on this topic, which is a must read for sessions lawyers.

The case, Mary Bradley v. Catherine A. Pesce, W2023-00583-COA-R3-CV (Tenn. Ct. Ap. Dec. 19, 2023)(full copy here), involves a lawsuit against two defendants, filed in general sessions court in 2020. Plaintiff served one defendant, but never got the other served. After taking a judgment in June 2022 against the served defendant, plaintiff nonsuited the claims against the never-served defendant in January 2023.

Using the date of the dismissal, the judgment defendant filed an appeal of the June 2022 judgment. The issue, of course, was whether her appeal was timely under Tenn. Code. Ann. § 27-5-108, which provides “[a]ny party may appeal from a decision of the general sessions court to the circuit court of the county within a period of ten (10) days.”

Wasn’t the defendant required to appeal within 10 days of the June 2022 judgment?

Looking to Tenn. R. App. P. 3(a), the Court of Appeals first asked whether a ruling in a matter is “final” where other claims (like a cross-claim) are still pending. The Court noted that the “finality rule” is applicable even in general sessions cases, citing other opinions that “the time for filing a notice of appeal [does] not begin to run until every claim raised in the general sessions court [is] adjudicated.” Further, the Court considered the 2018 amendments to Tenn. Code Ann. § 27-5-108, which provide that one party’s timely appeal takes all issues to the circuit court, even when other claims remain pending.

In the end, the Court concluded that because “the general sessions court action …was against two parties: Appellant and Ms. Weaver,” then “[t]he judgment against Appellant was not final and appealable until all the claims of all the parties were adjudicated,” and “[t]his occurred on or about January 5, 2023.” As a result, the appeal of the June 2022 ruling was not a final order until the dismissal order was signed.

In short, the concepts behind Rule 54.02 apply in Tennessee General Sessions Court, and litigants should keep this opinion in their mind any time a case involves multiple claims and parties.

Here, it seems like the judgment debtor acted out of necessity (and not by design). Frankly, the safest course of action would have been to file the appeal in June 2022 and be entirely certain that the appeal was timely (which would have, by operation of Tenn. Code Ann. § 27-5-108, taken the entire matter to circuit court).

On the other side of the aisle, an experienced plaintiff’s lawyer knows the incredible challenges that an evading or difficult-to-serve defendant presents, and that lawyer should take precaution to make any partial judgment final (and executable) as soon as possible.

This could be done in a few easy ways. The plaintiff could ask for text in the sessions judgment that tracks the language of Rule 54.02, making it clear that the order is a final order. The plaintiff could, at the time of the entry of the initial judgment, dismiss the other claims and parties. Or, if the other claims and parties were simply too crucial, the plaintiff could delay all relief or, at worst, live with a bit of ambiguity as to the finality of the partial judgment.

The appellate court’s reasoning is sound, but a savvy plaintiff has a number of ways to protect their client.

A more pressing question is this: If the “partial” sessions judgment isn’t final in a situation like this, then shouldn’t the Court Clerk refuse to issue execution? (Spoiler: Most will issue execution, but, based on this case, they shouldn’t.)

There are hardly any bankruptcy lawyers in Nashville under the age of 40.

With three law schools in the Middle Tennessee area, you’d think there’d be more than enough lawyers in Nashville to satisfy any and every conceivable legal need.

If so, you’d be wrong. In my recent experience, Nashville is an under-lawyered city, if you judge from the number of new calls I get (across the legal spectrum) and, as result, the difficulty I have finding a lawyer to refer these callers to.

As the country braces itself for an economic dip and you hear about law firm layoffs, I repeat my old advice: Learn Bankruptcy.

A bankruptcy practice is one of the best kept secrets in the profession. It’s all based on the Bankruptcy Code, which you can read cover-to-cover in an afternoon. It’s a small, collegial and sophisticated bar (the fact that it’s so small tends to prevent the shenanigans lawyers pull in the broader legal universe).

Plus, starting in a bankruptcy practice exposes you to nearly every legal issue imaginable, since so many state and federal law issues end up in bankruptcy court. Many complex transaction lawyers cut their teeth doing 363 sales in bankruptcy court.

During the last recession, Nashville was lucky and recovered quickly, with real estate prices rising, corporate growth, and a robust commercial lending base in the immediate years after the downturn.

The downside of that is that we’ve lost a generation of bankruptcy lawyers to corporate, commercial lending, and other (more sexy) practice areas. Today, in the year 2023, the lawyers who file debtor bankruptcies are largely the same ones who were filing those cases fifteen years ago. You can count the firms who file small/medium corporate chapter 11 cases on one hand.

I expect to see more national and local bankruptcy filings in 2024. If you’re a law student or recent grad trying to differentiate yourself from the pack, learning a little bit about bankruptcy law may be a smart move.

I have a question I ask clients when they ask me to foreclose on a property.

“Do you want the money or do you want the property?”

Some clients are baffled by the question. They are banks, they’ll tell me, and what are we going with a property? Who is going to evict the tenants, change the locks, make sure the pipes don’t burst, cut the grass and so on? The banks don’t want all that trouble. They want the money back, plain and simple.

But, in a hot real estate market like Nashville, I’ve noticed a new type of lender. I refer to them as “loan-to-own” lenders. They are making loans secured by real property, but they sometimes act like property investors.

My hunch is that, when making the decision to extend credit, the prospect of ending up owning the property is part of these lenders’ motivation in doing the deal. Hence, the “loan-to-own” nickname I give them. When their loans go bad, these lenders are happy to foreclose and take ownership of the land.

These are often lenders of last resort, for a property developer who can’t get credit (or more credit) from a traditional lender. These loans are often at far-above-market interest rates and usually on pretty short repayment terms. The typical customer is a developer who just needs a little bit more money or a bit more time, and who, out of desperation or arrogance, believes that the “big” sale is just 90-120 days away and is willing to overlook the costs and risks.

When the sale doesn’t happen or a payment is missed, these lenders pounce. In some cases, maybe the property developer can figure something out and the loan (and the hefty interest and fees) gets paid.

Or, worst case, the lender presses forward with a lender-advantageous foreclosure, i.e. one in which the lender who wants to win at the sale is the one who gets to set and enforce the sale terms.

Over the last few years, I’ve seen more lenders from Texas, Las Vegas, and California loaning money on development deals in Middle Tennessee. I’ve also noticed more of these lenders foreclosing, taking ownership, and then offering the properties for sale.

Having said all this, I don’t expect (or offer) much sympathy for the cash-strapped property prospectors. It’s simply an interesting development in the gold-rush ecosystem of the modern Nashville real estate market.