I represent a lot of landlords all over Tennessee. I also represent a lot of Tennessee small businesses who are, invariably, tenants.

Since COVID-19 hit, I’ve probably read 60 different leases. Sometimes, I’m looking at force majeure provisions or for ambiguities that would provide an argument against payment of rent. Other times, I am reading those same provisions (different leases) hoping for the opposite outcome.

Over the last 4 months, when scheduling my client calls, I’ve joked that “I do all my calls with my tenants in the morning, and I do all the landlord calls in the afternoon. I need to remember which argument to make.”

Even by lawyer standards, it’s rare to see such a equal distribution of misery on both sides of an issue.

So, today, when I read this New York Times Op-Ed, “The One Change That Could Save Your Neighborhood Stores,” I appreciated the generally even-handed approach to this nuanced topic.

The issue facing tenants?

[T]here’s no blueprint for how small-business owners should deal with their landlords during an economy-toppling pandemic.

Here’s one option: ignore your landlord and plan on resuming rent payments when sales hopefully improve, and try to not get evicted in the meantime. Another option? Stay current on rent and pray that the economy recovers before you run out of cash.

Neither one of these options are really good, but the tenant doesn’t have any better options. Making matters worse, the Bankruptcy Code isn’t much help, unless the lease assumption statute gets changed, to provide relief to tenants:

One possible solution is that Congress temporarily change bankruptcy law so that small businesses can be allowed to pay their landlords more reasonable amounts until the pandemic is behind us.

Some quick background: Under the Bankruptcy Code, a Chapter 11 debtor can generally stop paying its creditors during the time the case is pending and, even after a plan of reorganization is confirmed, that plan may provide drastically modified (reduced) payments to its creditors.

That’s not the case with landlords, though: Under 11 U.S.C. Section 363 of the Bankruptcy Code, landlords are entitled to demand their full monthly rent due the entire time, and, in order for a lease to be included in a bankruptcy plan, the landlord must be paid current. Long story short, a tenant’s bankruptcy filing is a temporary speed bump for landlords, but the path to payment in full for a landlord is pretty direct.

As a result, many landlords have been aggressive during the pandemic, emboldened by state and federal law. The article mentions that many landlords are starting to see the writing on the wall (and that, maybe, there aren’t any replacement tenants) and are considering “pay what you can” agreements.

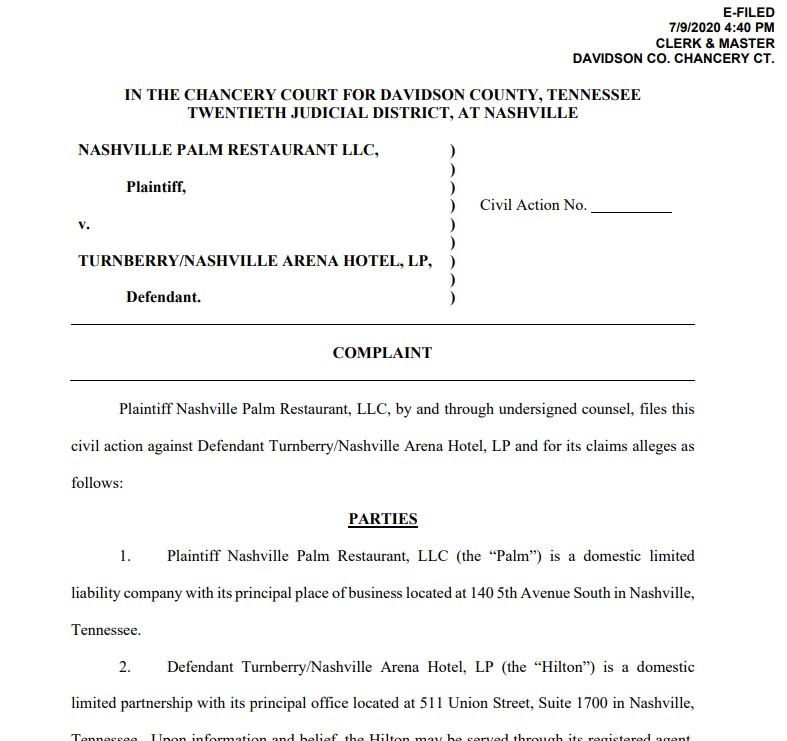

States have offered limited help to tenants, in the form of moratoriums on evictions (though such efforts are not reducing or stopping the financial payment obligations for the accruing rent). Plus, deep-pocketed large retailers are cooking up some innovative legal arguments (the article cites Valentino and Victoria’s Secret, but it could have also cited the Nashville lawsuit filed by The Palm Restuarant against the Nashville Hilton).

To the landlord’s defense, the article notes that landlords, themselves, may be small entrepreneurs with mortgages of their own and who depend on the rental income stream. The article advocates for tax cuts for commercial lessors.

Again, the article presents a fairly even-handed consideration of a “no win” situation. If the landlords win, then thousands of small businesses go under in the next 6 months.

As for the landlords, it’s just one of many problems facing them during the pandemic. This Reuters article’s title says it all: Who still needs the office? U.S. companies start cutting space.

(Note for the non-Sheikhs out there: Retail value for new G5s can be between $36MM and $48MM).

(Note for the non-Sheikhs out there: Retail value for new G5s can be between $36MM and $48MM).